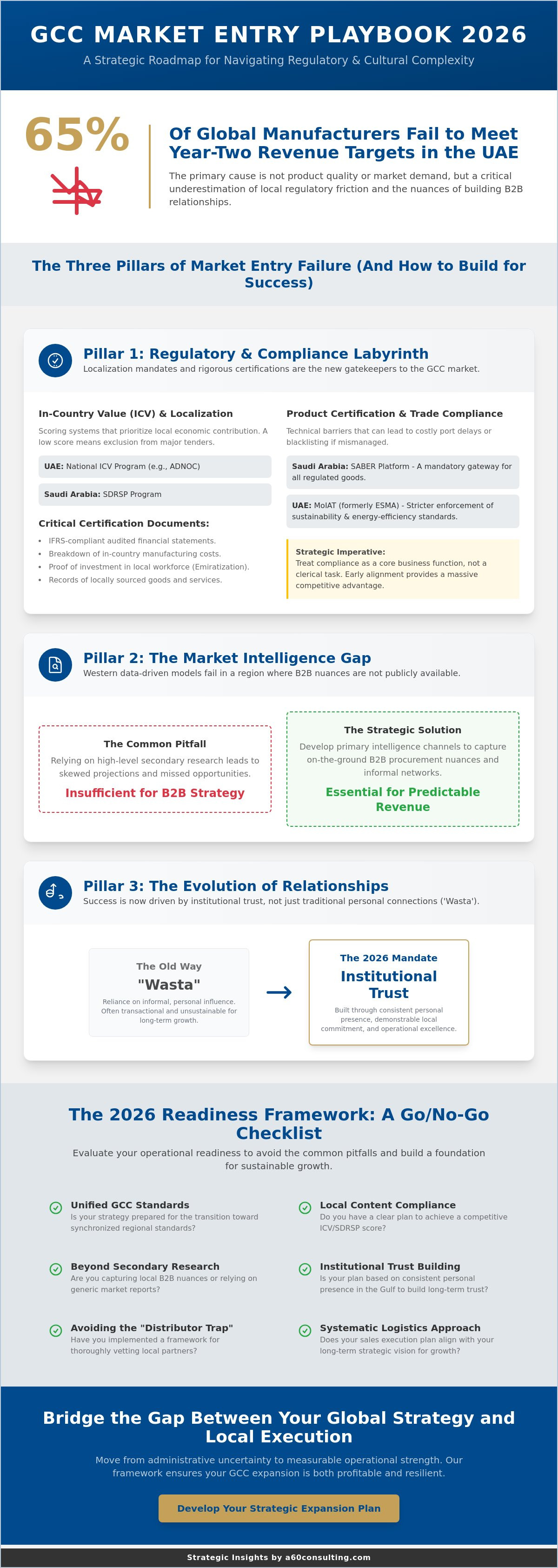

Did you know that 65% of global manufacturers fail to hit their year-two revenue targets in the UAE because they underestimate the depth of local regulatory friction? While the GCC offers a high-growth environment, many firms find that a standard expansion playbook fails to account for the specific market entry challenges middle east territories present to newcomers. You've likely felt the frustration of opaque compliance hurdles or B2B sales cycles that stretch far beyond your initial projections. It's a common struggle, but it's one that can be managed with the right structural approach and a shift in strategic perspective.

This guide provides a clear, 2026-ready roadmap for compliance and sustainable growth. We'll outline a proven framework for vetting local partners, navigating MoIAT standards, and building the personal trust necessary to turn long sales cycles into predictable revenue streams. By applying these strategic filters, you'll move from administrative uncertainty to a position of measurable operational strength. Our goal is to bridge the gap between your global strategy and local execution, ensuring your expansion is both profitable and resilient.

Key Takeaways

- Understand the transition toward unified GCC standards and why strict local content requirements have become the primary barrier for industrial and tech firms.

- Identify how to navigate the region's opaque data landscape by moving beyond secondary research to capture essential local B2B nuances.

- Learn to bridge the cultural gap by evolving your strategy from traditional 'Wasta' to building institutional trust through consistent personal presence in the Gulf.

- Evaluate your readiness using a 2026 Go/No-Go framework designed to navigate the most critical market entry challenges middle east and avoid the common "distributor trap."

- Develop a systematic approach to operational logistics that ensures your sales execution matches your long-term strategic vision for sustainable growth.

Navigating Regulatory Complexity and Local Content Requirements

The regulatory environment across the Gulf Cooperation Council (GCC) is undergoing a fundamental transformation. By 2026, we anticipate a more synchronized set of standards, yet the push for industrial sovereignty has made local content mandates more stringent. For industrial and tech firms, these regulatory hurdles represent the primary market entry challenges middle east operators must overcome. Success no longer depends solely on product quality. It hinges on your ability to integrate into the local economic fabric. You'll find that the Economy of the Middle East is increasingly defined by localization as a prerequisite for participation in large-scale projects.

This shift requires a move from a pure export model to a partnership-driven approach. Our 2026 GCC Market Entry Strategy: A Blueprint for Strategic Regional Expansion provides a detailed framework for this transition, emphasizing that regulatory alignment is the foundation of any sustainable growth plan. We see that firms ignoring these shifts face exclusion from the most lucrative government tenders in the UAE and Saudi Arabia.

Understanding In-Country Value (ICV) and SDRSP

Saudi Arabia and the UAE have moved beyond simple preference for local firms. They now use sophisticated scoring systems like the National ICV Program in the UAE and the Strategic Development and Regional Supply Chain Program (SDRSP) in Saudi Arabia to vet international suppliers. If your ICV score is low, your chances of winning a government tender or a contract with entities like ADNOC are virtually zero. Early compliance provides a massive strategic advantage, often outweighing price competitiveness in the final evaluation. To secure a competitive score, you'll need specific documentation for certification:

- Certified audited financial statements prepared according to IFRS standards.

- A detailed breakdown of manufacturing costs incurred within the UAE.

- Third-party verification of investment in local workforce development and Emiratization targets.

- Documentation of locally sourced goods and services from other certified suppliers.

- Verified records of export revenue generated from your local manufacturing base.

Product Certification and Trade Compliance (SABER & ESMA)

Technical barriers are equally demanding. In Saudi Arabia, the SABER platform is the mandatory gateway for all regulated consumer and industrial goods. It's not just a portal; it's a rigorous verification process that requires deep technical documentation. In the UAE, the evolution of ESMA standards into MoIAT (Ministry of Industry and Advanced Technology) frameworks for 2026 means stricter enforcement of sustainability and energy-efficiency metrics. Conformity Assessment acts as the non-negotiable gatekeeper to regional customs, ensuring every imported unit aligns with rigorous safety and quality benchmarks. Mismanaging these certifications leads to costly port delays and potential blacklisting. You should treat compliance as a core business function rather than a clerical task, as the market entry challenges middle east presents are often won or lost at the customs border.

Overcoming Market Intelligence and Data Transparency Gaps

Entry into the Gulf Cooperation Council (GCC) often reveals a stark reality; the data-driven clarity found in Western markets doesn't exist here in the same format. Western markets rely on accessible databases like Companies House or the SEC, but in the UAE, private company financials remain largely confidential. This opacity is one of the primary market entry challenges middle east newcomers face when building their financial models. Relying on secondary research or high-level reports often leads to skewed projections because these documents miss the ground-level nuances of B2B procurement.

A specialized Saudi Arabia Business Development Agency for Tech provides the necessary field data to bridge these gaps, especially as cross-border trade between Dubai and Riyadh intensifies. Understanding these nuances is one of the Keys to Business Success in the Middle East, as relationship-based intelligence often outweighs public reports. Without real-time field data, companies risk entering the market with a value proposition that doesn't resonate with local decision-makers who prioritize long-term stability over short-term cost savings.

The B2B Market Sizing Challenge

Top-down market sizing fails for complex product manufacturers in the region. A company might see a massive infrastructure budget of 180 billion AED and assume a 1% market share is easily attainable. This logic is flawed. In the GCC, "market share" is often locked behind government-linked entities and specific family-owned conglomerates. Localized validation is the only way to uncover hidden demand in government-led projects like the UAE's Operation 300bn. Using local interviews to verify the actual pipeline of projects ensures that your 2026 revenue targets are based on reality rather than optimistic spreadsheets.

Vetting Competitors and Pricing Strategies

Identifying "shadow" competitors is critical. These are local players who might not have a sophisticated digital presence but hold significant market share through legacy relationships and deep-rooted trust. They don't list their prices online, making benchmarking difficult. In a market where tenders can fluctuate by millions of AED, value-based pricing is your strongest tool. Instead of competing for the lowest bid, successful entrants demonstrate how their solution reduces operational costs over a five-year period. Feasibility studies conducted by a strategic partner can prevent the costly mistake of over-investing in a saturated niche where legacy players cannot be easily displaced.

- Data Verification: Cross-reference secondary reports with at least 15-20 local industry stakeholder interviews.

- Competitive Intelligence: Focus on "unseen" local incumbents rather than just international peers.

- Pricing Models: Shift from "cost-plus" to "total cost of ownership" to justify higher entry prices in AED.

Strategic success in 2026 requires moving beyond the surface. When data isn't transparent, your competitive advantage lies in your ability to gather what others cannot see. This transition from "guessing" to "knowing" transforms a high-risk gamble into a calculated expansion.

Bridging the Cultural Gap: The Evolution of 'Wasta' and Relationships

Success in the UAE no longer depends on opaque backroom deals; it relies on a sophisticated fusion of institutional credibility and personal rapport. As we approach 2026, the traditional concept of 'Wasta' has transitioned from simple nepotism to a professionalized form of networking. One of the primary market entry challenges middle east newcomers face is underestimating this shift. Influence today is earned through a track record of reliability and a visible commitment to the Emirates' long-term goals, such as the 'We the UAE 2031' vision. Decision-makers now seek partners who can align their global expertise with the specific socio-economic fabric of the Gulf.

Relationship-Driven Sales vs. Transactional Pitching

Western firms often arrive with a polished 15-minute deck, expecting a decision by the end of the hour. In the Gulf, the first three meetings are rarely about the product's technical specifications. They function as a vetting process for your character and resilience. You're expected to demonstrate 'patience capital', which is the willingness to invest time before demanding a signature. To adapt your pitch for GCC decision-makers, focus on how your solution supports national prosperity rather than just your internal ROI. If you can't show how you'll be here in five years, the conversation likely won't progress past the initial coffee. Personal presence remains the currency of B2B sales; virtual meetings cannot replace the 'Face' required to close high-value contracts in Dubai or Abu Dhabi.

The Role of Local Representation

A common mistake is treating local representation as a mere legal checkbox. While a legal sponsor fulfills a regulatory requirement, a strategic business development partner provides the 'local face' necessary to navigate complex stakeholder ecosystems. In the 2026 landscape, we define 'Wasta' as the bridge of trust between global innovation and local needs. This bridge requires more than just English-only sales collateral. Although 90% of private sector business in Dubai happens in English, hyper-localization is the new standard for corporate communication.

- Hyper-localization: By 2026, 70% of government-linked entities will prioritize partners who provide dual-language technical documentation.

- Physical Presence: Relying on a London or New York-based team to manage daily relations often leads to a disconnect that local competitors will exploit.

- Cultural Currency: Understanding the nuances of Majlis culture can accelerate procurement cycles by months.

Effective market entry requires a physical presence that signals you're a stakeholder in the region's future, not just a transient service provider. Strategic depth in your communication, including localized Arabic digital footprints, demonstrates a level of respect that transcends the transactional nature of a standard sales pitch. This approach builds the institutional trust required to secure long-term contracts in a competitive 2026 market.

Operational Logistics and Sales Execution Hurdles

Transitioning from a strategic plan to active sales execution in the United Arab Emirates reveals the true complexity of the region. Many organizations underestimate the "last mile" of operations, assuming that a high-quality product will naturally find its way through local channels. Addressing the core market entry challenges middle east requires a shift from HQ-centric thinking to a localized, hands-on management style that accounts for extended timelines and high-touch relationship management. The reality of managing a sales pipeline from 5,000 kilometers away often leads to communication gaps that local competitors quickly exploit.

Managing the Long Sales Cycle

Industrial and enterprise software contracts in the GCC typically follow a 12 to 24-month trajectory. For projects exceeding AED 3,500,000, the procurement process involves multiple layers of technical committees and financial audits. Maintaining momentum during these gaps is critical. Successful firms implement interim milestones, such as paid feasibility studies or pilot programs, to keep local stakeholders engaged. These smaller wins provide the necessary data to justify the final investment to senior Emirati decision-makers while preventing the lead from going cold during summer months or religious holidays when decision-making naturally slows down.

Distributor Management and Performance Vetting

The "Distributor Trap" is perhaps the most common pitfall for foreign manufacturers. Signing a partnership agreement represents only 10% of the effort required for market success. Many regional distributors manage extensive portfolios and will naturally gravitate toward the easiest sale. Without active sales enablement and co-selling, your product may sit dormant in their catalog for years. Middle Eastern distributors often "under-perform" because they lack the specific technical training or the marketing budget to create demand independently.

Performance vetting must be continuous rather than annual. You need to ensure your partner isn't just a "trophy collector" but an active extension of your sales team. To avoid these pitfalls, follow the vetting protocols outlined in our Strategic Guide to Distributor Search in the Middle East. Structuring agreements with clear, quarterly KPIs and mandatory "joint sales calls" ensures accountability and prevents the relationship from becoming stagnant.

Recruitment for specialized technical roles in hubs like Dubai and Abu Dhabi adds another layer of difficulty. A Senior Solutions Architect often commands a monthly salary of AED 45,000 to AED 60,000, excluding the costs of residency visas and mandatory medical insurance. With regional talent turnover rates in the tech sector occasionally reaching 25%, businesses must build robust knowledge-sharing systems. Relying on a single "star" employee without a documented implementation process creates a significant risk to long-term stability. Overcoming these market entry challenges middle east demands a balance between finding top-tier talent and building organizational resilience that survives individual departures.

The 2026 Middle East Market Entry Checklist

Success in the UAE market by 2026 hinges on your ability to move from abstract strategy to precise execution. The landscape has matured; the introduction of the 9% corporate tax in June 2023 and the tightening of In-Country Value (ICV) requirements mean that "winging it" is no longer a viable path. Addressing market entry challenges middle east requires a systematic approach that balances regulatory compliance with high-stakes relationship building. Before committing capital, use this Go/No-Go framework: if you can't verify a local demand for your specific price point or navigate the MoIAT (Ministry of Industry and Advanced Technology) standards, your entry is premature.

Phase 1: Strategic Feasibility and Compliance

The first phase focuses on removing assumptions. You must verify product-market fit not through desktop research, but through at least 15 to 20 local B2B interviews with key stakeholders in Dubai or Abu Dhabi. These conversations reveal the nuances that data sheets miss. Simultaneously, you need to map out your regulatory roadmap. This includes identifying if your products require SABER certification for regional trade or specific registration with the UAE Ministry of Health and Prevention.

- Financial Audit: Compare the cost of a Free Zone setup (averaging AED 15,000 to AED 50,000) against a Mainland license, factoring in the 2026 requirements for physical office space.

- ICV Readiness: Assess your potential In-Country Value score. In 2025, companies with higher ICV scores secured 35% more government-linked contracts than those without.

- Entry Mode Analysis: Determine if a local distributor or a Joint Venture is more cost-effective than a 100% foreign-owned subsidiary.

Phase 2: Local Alliance and Sales Execution

Once the foundation is set, the focus shifts to the "trust" factor. In the UAE, business is personal. Identifying and vetting top-tier distribution partners requires a weighted scorecard that evaluates their technical capability, financial health, and existing relationships with procurement heads. Don't rely on a single partner for the entire GCC; local expertise in Abu Dhabi can differ significantly from Dubai or Sharjah.

- Physical Presence: Establish a local representative or a "light" office. Decision-makers in the UAE rarely close major deals with entities that don't have a local landline and a physical footprint.

- Sales Enablement: Adapt your global tech stack to local procurement cycles, which often peak between October and December.

- Regional Comparison: Use this Strategic Guide for Market Entry to compare UAE's operational costs against other regional hubs.

Navigating market entry challenges middle east is an exercise in discipline. At A60 Consulting, we don't just hand you a report; we manage the execution side of this checklist. We act as your on-the-ground partner to ensure that your strategy translates into measurable revenue. Whether it's vetting partners or navigating the MoIAT registration process, we bridge the gap between your global vision and local reality.

Converting Strategic Intent into GCC Market Growth

Thriving in the Gulf requires more than a standard expansion plan; it demands a precise alignment with the region's rapid regulatory shifts. By 2026, navigating market entry challenges middle east will focus heavily on meeting local content requirements like the UAE's In-Country Value (ICV) program, which now influences billions in procurement. Success isn't just about understanding the rules. It's about bridging the gap between strategic vision and the operational realities of the local industrial and software landscape. You'll need to balance the traditional importance of deep-rooted relationships with the transparent, data-driven expectations of modern GCC enterprises.

A60 Consulting brings 30+ years of regional sales leadership to your expansion. Our team has a proven track record delivering on complex Saudi Vision 2030 projects and specialized industrial GTM strategies. We don't offer generic advice. We provide the structural discipline needed for measurable results in the Emirates and beyond. Schedule a strategic consultation with A60 Consulting to navigate your GCC entry challenges and ensure your 2026 roadmap is built on professional expertise rather than guesswork. The opportunity for growth is substantial for those ready to execute with precision.

Frequently Asked Questions

What are the biggest market entry challenges in the Middle East for tech companies?

Navigating data residency requirements and localized compliance frameworks represents the primary hurdle for international firms. Tech companies must align with the UAE Federal Decree-Law No. 45 of 2021, which mandates strict protocols for personal data processing. These market entry challenges middle east often involve technical adjustments to ensure cloud infrastructure remains within national borders. Success depends on adapting software architecture to meet these specific regional security standards early in the process.

How long does it typically take to enter the GCC market in 2026?

Establishing a fully operational presence takes between 6 and 12 months for most organizations. While digital platforms like "Invest in Dubai" permit license issuance in minutes, the subsequent steps require significant patience. Opening a corporate bank account and securing employee visas involve rigorous compliance checks that consume 3 to 5 months. Planning for this timeline ensures your capital reserves remain stable during the pre-revenue phase of the implementation.

Is it possible to sell in the Middle East without a local office?

You can reach customers through cross-border e-commerce platforms or third-party distributors without a physical footprint. However, the UAE Commercial Companies Law requires a local entity for most government procurement and large-scale B2B contracts. Selling remotely limits your ability to provide immediate after-sales support or build deep institutional trust. This often leads to lower conversion rates compared to competitors who maintain a boots-on-the-ground presence.

What is the role of a local partner in the UAE and Saudi Arabia?

Local partners act as strategic bridges to regulatory bodies and high-value commercial networks. Although the UAE now allows 100% foreign ownership for over 1,000 commercial activities, a partner provides essential market intelligence. In Saudi Arabia, partners help navigate the "Nitaqat" labor nationalization program and cultural nuances. They don't just hold equity; they facilitate the influence needed to bypass bureaucratic bottlenecks and accelerate growth.

How do I protect my intellectual property when entering the GCC?

Register your trademarks and patents directly with the UAE Ministry of Economy to ensure full legal enforcement. Since the UAE joined the Madrid Protocol in 2021, international applicants can streamline this process more efficiently. Don't rely on home-country registrations, as IP rights remain strictly territorial in the region. Local registration provides the only guaranteed protection against counterfeit goods and unauthorized usage in the regional marketplace.

What is the In-Country Value (ICV) certificate and do I need it?

The ICV certificate measures a company's contribution to the local economy and is vital for government tenders. Entities like ADNOC and the Abu Dhabi Department of Economic Development use this score to rank bidders during procurement. If you're targeting the public sector or the energy industry, a high ICV score is mandatory. It rewards companies that hire local talent and source materials from within the UAE borders.

How much does a market entry strategy for the Middle East cost?

Initial licensing costs in UAE free zones typically range from 12,500 AED to 50,000 AED depending on the specific jurisdiction and activity. This figure excludes office rent, visa deposits, and professional consultancy fees. Comprehensive market entry challenges middle east include hidden costs like mandatory health insurance and legal translations of corporate documents. Budgeting at least 150,000 AED for the first year's operational setup is a realistic baseline for most SMEs.

Can I use one distributor for the entire GCC region?

It's legally permissible to appoint a single distributor, but it's rarely the most efficient strategy for sustainable growth. Each GCC member state has unique customs regulations and distinct consumer preferences. For instance, Saudi Arabia’s Regional Headquarters program incentivizes companies to set up direct hubs in Riyadh. Using separate partners for the UAE and Saudi markets often yields 30% higher growth rates through specialized local expertise.